The Factors That Determine Your Pre-Approval Amount

You're nervously gathering the documents to upload into a lender's portal, wondering if this will be enough to get pre-approved for the amount you want.

What determines your pre-approval amount? Will the information you give increase or reduce the amount you get?

All good questions, but let's get something straight:

Your pre-approval is decided by your income and anything that impacts it.

Lenders build a profile based on your record and finances to help them decide how much to lend you and the details of that loan.

So what are some things lenders factor in?

We at Savant Realty Group researched a list of items a lender will pull to build your profile and your loan amount. This profile includes (but is not limited to) your identification and background check, your employment history and tax returns, and your financial info.

Identification and Background Check

Lenders want to make sure that you are who you say you are and for any history.

If you have a criminal background, that should not deter you from getting a mortgage. Most lenders will still give you a loan as long as your finances show that you're not a high-risk borrower.

Some lenders may give you a higher APR% or deny you outright, but that is not as common.

We recommend that you shop lenders as every potential home buyer should. It allows you to pick the best pre-approval or leverage options to get the best deal.

Employment & Tax Returns

Lenders mainly check your financial health, and income is the first insight.

To get a good idea of your total income and its stability, lenders will review your employment history and tax returns.

Employment History

To get a clear idea of your employment history, lenders will look at your employment status, how long you have worked at the same company, and how much you make.

What lenders see:

- Being employed shows lenders that you have a steady stream of income that comes in monthly

- Having the same job for an extended period will let the lender know this employment and income will be long-term.

- Lenders may ask for pay stubs from the last three months to ensure that income doesn't fluctuate.

Tax Returns

A lender may ask for your tax returns, especially if you are self-employed or have multiple sources of income.

Tax returns show your total income within a year, not just what you make from your day job.

Loan officers will require the last two consecutive years of your tax returns, so make sure you file taxes correctly and on time.

Financial Info

The next part of your financial health that lenders look at is the details of your finances.

Lenders will look at your credit score, credit history, debt-to-income ratio, and savings & assets.

Credit Score

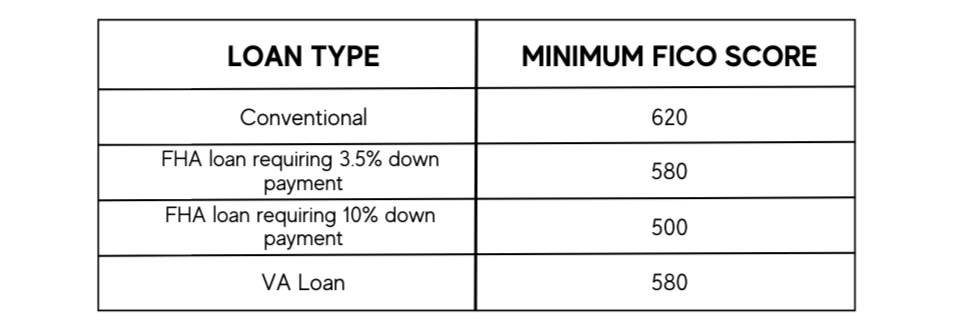

Your credit score will qualify you for different types of loans. At Savant Realty Group, we recommend maintaining at least a score of 640 or above. However, we have included the loans and the qualifying scores for each.

Credit scores will also impact the interest rate of your mortgage loan. Borrowers with higher FICO scores benefit from lower rates, thus spending less on repaying the loan.

Credit History

Lenders will also look at your credit history to get the full story behind your credit score.

Is your credit score on the lower end because you constantly max out your credit cards? Because you regularly make payments late? Due to accounts ending up in collections? All of the above? (source)

Or is it simply because you don't have enough credit history in the first place?

A mortgage lender will run a fine-tooth comb through your credit history to decipher what kind of borrower you will be. It solidifies their decision on whether to lend you money and the amount and rate to give you.

Debt-To-Income Ratio

The Debt-To-Income Ratio is a ratio used by all lenders to evaluate your ability to make your monthly payments.

To determine your DTI, lenders take your monthly debt and divide it by your monthly income. They multiply that number by 100 to get a percentage. If the said percentage is under 36% when your DTI is determined, it's best.

Lenders use DTI to assess the risk of giving you money to buy your home.

Saving and Assets

Your lender will review your savings and assets to determine your net worth.

They will subtract the value of your savings assets from your debts to estimate how much money you have, so it's important to be forthright.

It also affords them a sense of security if you lose your primary source of income by showing you can continue to make your payments correctly and on time (source).

Conclusion

So let's recap:

Your pre-approval amount is defined by your income and whatever impacts it.

Lenders will build and review a profile that creates a complete picture of this by looking over your identification and doing a background check, understanding your income through your employment history & tax returns, and comprehending what impacts that income by looking at your financial info.

It's your job that these factors boost your prospects of getting pre-approved for the amount you want.

If you're unsure where to start or want to contact a lender to either get pre-approved or develop a game plan, then schedule a time to speak with us.

We'll give you the advice and resources to make the best decisions throughout your real estate journey.

Categories

- All Blogs (659)

- Affordability (16)

- Agent Value (27)

- Baby Boomers (8)

- Buyers (437)

- Buying Myths (117)

- Buying Tips (49)

- Credit (3)

- Demographics (32)

- Distressed Properties (6)

- Down Payment (23)

- Downsize (2)

- Economy (16)

- Equity (12)

- Family (2)

- Featured (8)

- First Time Homebuyers (211)

- For Sale by Owner (1)

- Forecasts (7)

- Foreclosures (28)

- FSBOs (11)

- Gen X (1)

- Gen Z (5)

- Home Improvement (2)

- Home Prices (37)

- Housing Market Updates (231)

- Interest Rates (70)

- Inventory (30)

- Investing (6)

- Kids (2)

- Leasers (6)

- Lenders (4)

- Loans (8)

- Luxury Market (3)

- Market (3)

- Millennials (9)

- Mortgage (18)

- mortgage rates (31)

- Move Up Buyers (84)

- New Construction (13)

- Pricing (95)

- Rent v. Buy (36)

- Self-Employed (1)

- Sellers (292)

- Selling Myths (87)

- Selling Tips (40)

- Senior Market (1)

Recent Posts

GET MORE INFORMATION

Agent | License ID: 740140